(19.) Use only technology (no formulas), preferably the TVM app in the TI-series calculators to solve

these questions.

Show the screenshots of your solutions.

Interpret your answers in the context of the question.

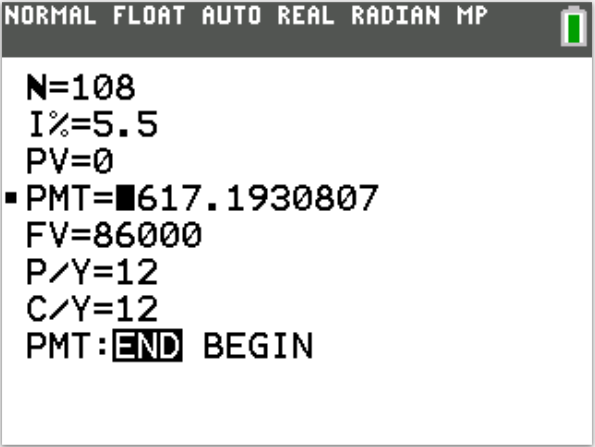

(I.) You want to purchase a new car in 9 years and expect the car to cost $86,000.

Your bank offers a plan with a guaranteed APR of 5.5% if you make regular monthly deposits.

How much should you deposit each month to end up with $86,000 in 9 years?

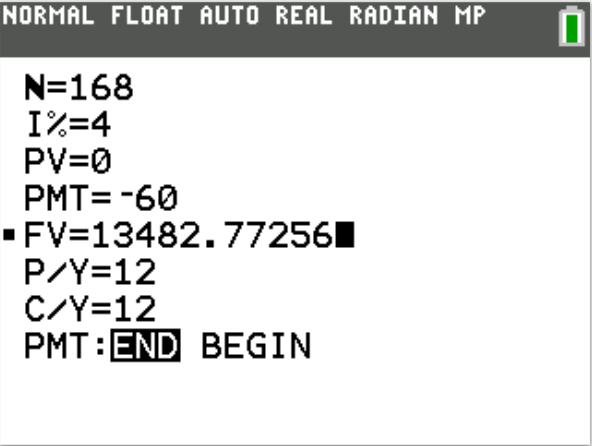

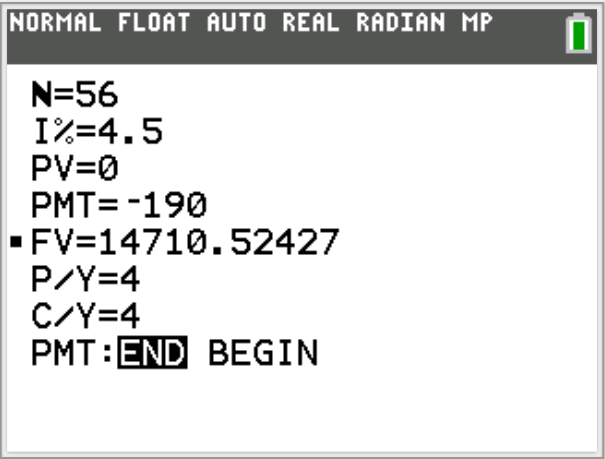

(II.) Consider the pair of savings plans below.

Hannah deposits $60 per month in an account with an APR of 4%, while Sarah deposits $190 per quarter in an account with an APR of 4.5%.

Compare the balances in each plan after 14 years.

(I.) This is a case of Sinking Funds

$N = mt = 12 * 9 = 108$

You should invest $617.19 each month.

(II.) This is a case of Future Value of Ordinary Annuity

Hannah: $N = mt = 12 * 14 = 168$

The balance in Hannah's account is $13482.77

Sarah: $N = mt = 4 * 14 = 56$

P/Y = 4

C/Y = m = 4

The balance in Sarah's account is $14710.52

Show the screenshots of your solutions.

Interpret your answers in the context of the question.

(I.) You want to purchase a new car in 9 years and expect the car to cost $86,000.

Your bank offers a plan with a guaranteed APR of 5.5% if you make regular monthly deposits.

How much should you deposit each month to end up with $86,000 in 9 years?

(II.) Consider the pair of savings plans below.

Hannah deposits $60 per month in an account with an APR of 4%, while Sarah deposits $190 per quarter in an account with an APR of 4.5%.

Compare the balances in each plan after 14 years.

(I.) This is a case of Sinking Funds

$N = mt = 12 * 9 = 108$

You should invest $617.19 each month.

(II.) This is a case of Future Value of Ordinary Annuity

Hannah: $N = mt = 12 * 14 = 168$

The balance in Hannah's account is $13482.77

Sarah: $N = mt = 4 * 14 = 56$

P/Y = 4

C/Y = m = 4

The balance in Sarah's account is $14710.52